Expert Lending For Real Estate Investors

Unlock Your Investment Potential

“Zig when others zag” – We see

opportunity where others see obstacles.

Pinnacle Lending Partners is a forward-thinking financial services firm dedicated to empowering individuals, families, and businesses through innovative lending solutions. At Pinnacle Lending Partners, we specialize in private money lending for non-owner-occupied single-family and commercial real estate investments. Our mission is simple: to provide access to capital that drives growth, opportunity, and long-term financial well-being by redefining lending through financial expertise and a client-first approach—ensuring every borrower feels empowered, supported, and confident in their financial journey.

We fund real estate investors nationwide with flexible financing solutions tailored to their needs. Based in Silicon Valley, California, our dedicated team understands market dynamics and works diligently to provide quick funding, helping you seize opportunities and close deals confidently and quickly. Investors partner with us to elevate their real estate investments to new heights.

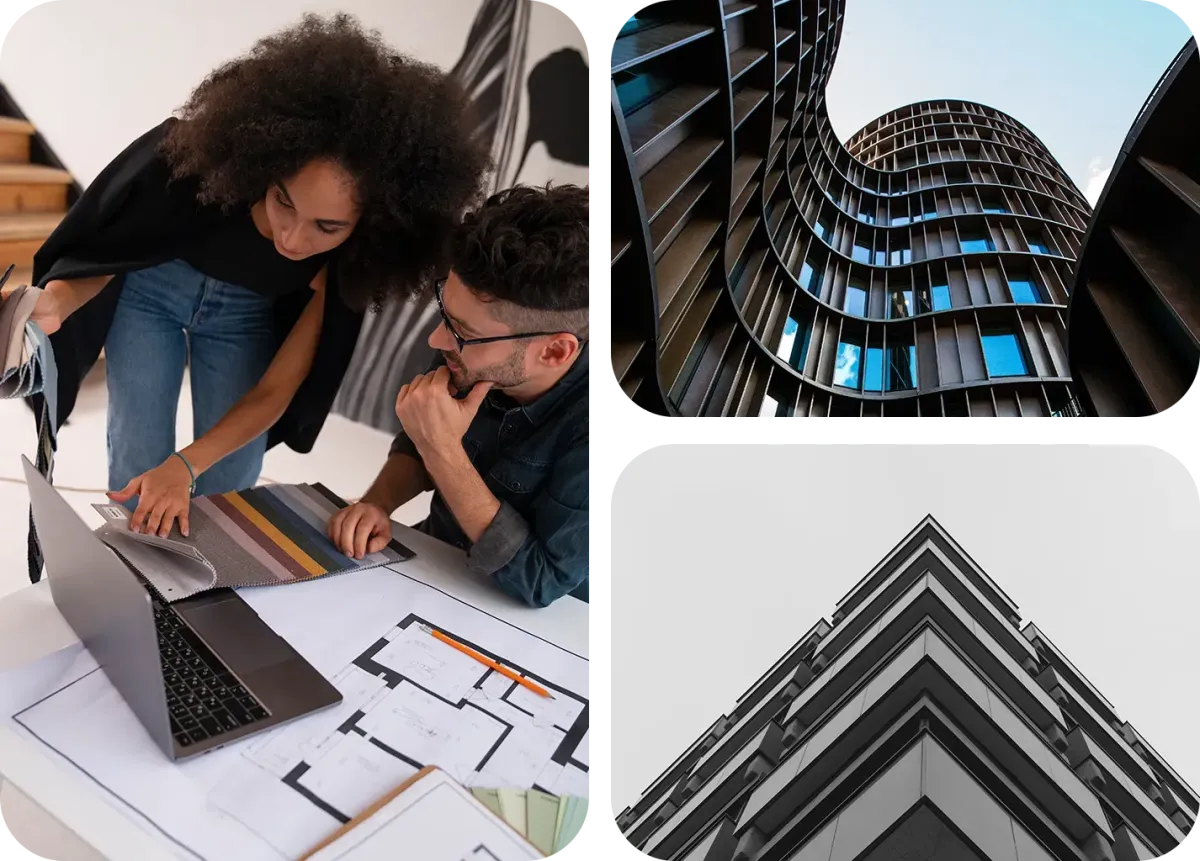

Our Services

From vision to closing, we provide flexible lending solutions designed to bring your real estate investment goals to life.

Fast Financing Solutions

Quick and effective financing options for investors.

Flexible Loan Structures

Customizable loans to suit your investment strategy.

Expert Guidance and Support

Dedicated support and expertise for investors.

Why Choose Us

Our Approach

We combine the entrepreneurial spirit of innovators with the discipline of seasoned financial leaders. Our unique value lies in our ability to:

Design lending solutions that align with client needs, not cookie-cutter products.

Leverage technology to streamline applications, approvals, and closings.

Provide market insight and advisory, not just financing.

Client Stories

REAL STORIES FROM OUR VALUED CUSTOMERS

Pinnacle Lending Partners has completely transformed the way I approach real estate investing. Their fast and flexible funding options allowed me to seize opportunities I would have otherwise missed. The team is knowledgeable and always ready to help, guiding me through the entire process with ease. Every deal I’ve closed with their assistance has been a game changer for my portfolio. If you're serious about investing, I can't recommend them enough!

Working with Pinnacle Lending Partners has been a breath of fresh air in the often-stressful world of real estate. The speed of their loan approvals and the clarity of their terms made my last property acquisition seamless. Their team provided excellent support and was always available to answer my questions. I appreciate how they genuinely care about their clients' success, making my investment journey not just profitable but enjoyable. They truly stand out in the lending industry!

I’ve worked with several lenders over the years, but Pinnacle Lending Partners is by far the most reliable and efficient. Their professionalism and excellent communication made the process smooth from start to finish. I was able to close on my latest investment property quickly, thanks to their tailored lending solutions. They understand the unique challenges of real estate investing and are committed to finding the best financing options. If you want a partner that truly understands your needs, look no further than Pinnacle Lending Partners!

Innovation

Fresh, creative solutions.

Integrity

Honesty and transparency.

Excellence

Top-notch services.

FOLLOW US

LEGAL

Copyright 2026. San Francisco, CA. All Rights Reserved.